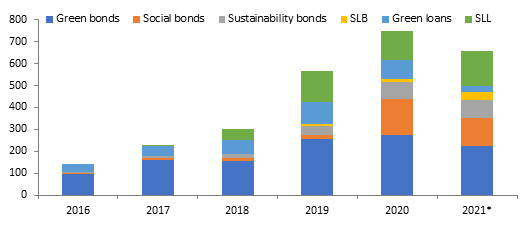

The issuance of sustainable debt has skyrocketed globally to reach a record volume of over $700bn in 2020 with the growing importance of Environmental, Social, and Governance (ESG) financing. ESG bond issuances in the first half of 2021 is set to surpass the 2020-levels and could easily hit $1tn for the year at the current rate. Green bonds remain the most popular within the sustainable debt basket. However, sustainability-linked bonds (SLBs) have witnessed significant momentum bolstered by the introduction of Sustainability-Linked Bond Principles (SLBP) by the International Capital Market Association (ICMA) in June 2020. Despite being the smallest subset of the sustainable debt basket (2% in 2020), sale of SLBs stood at $34bn during the first half of 2021, up from $16bn and $9bn seen in 2020 and 2019, respectively. In the same vein, social bonds too deserve a special mention given the exceptional rise (700% y/y) in issuances in 2020. This rise is attributed to the investors’ focus on the “social” component driven by increased borrowing from governments and companies, given the pandemic.

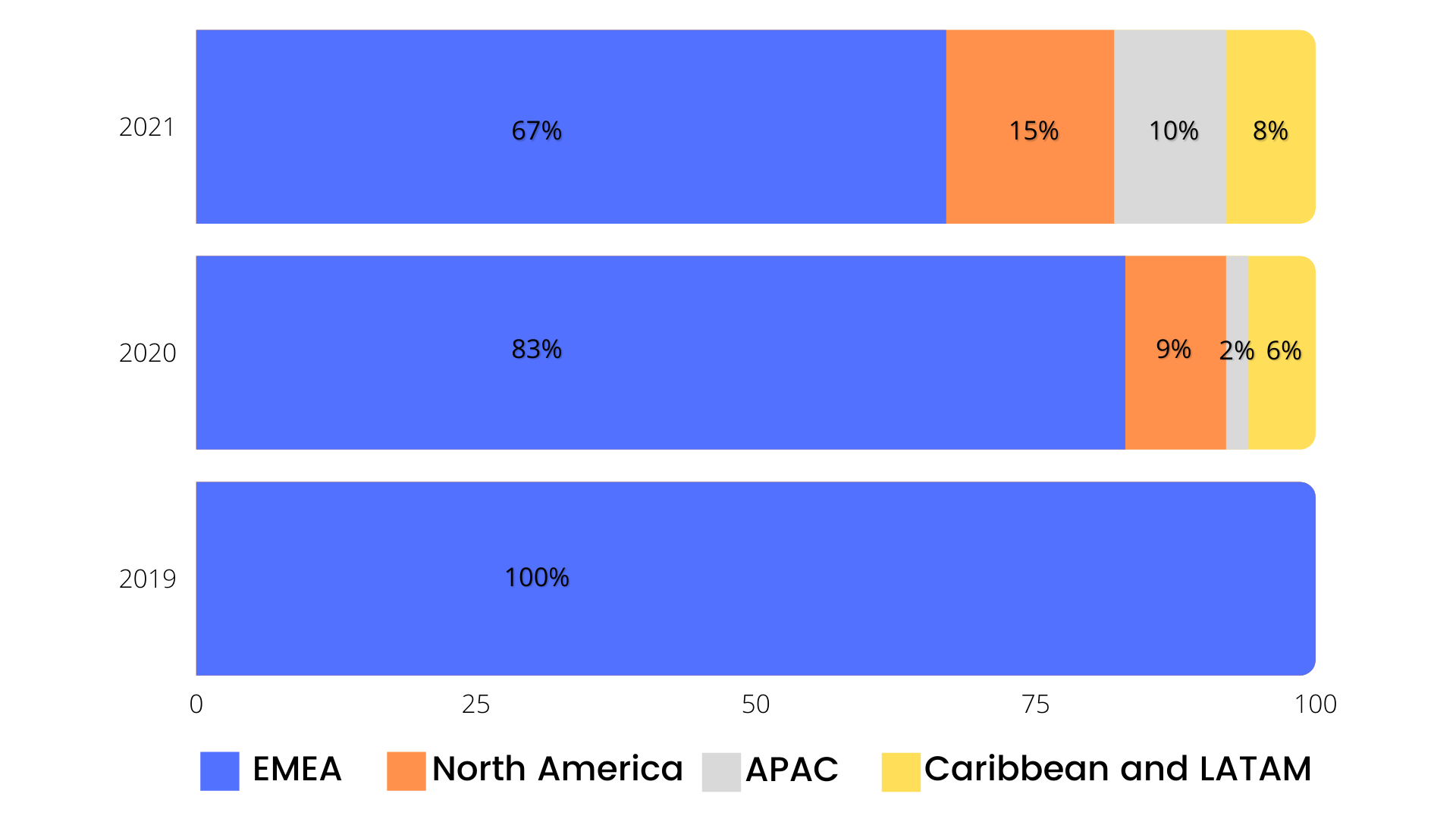

Sales of ESG debt by asset type ($bn)

Source: Bloomberg (*Data through June 11, 2021) Note: SLL=Sustainability-linked loans

SLBs can become the issuers’ favorite on structural flexibility

SLBs are the first of its kind KPI-linked instrument in the ESG debt space that emerged in 2019. In SLBs, borrowers assign ESG-specific targets to their issuances, which if not met, would attract penalties. Rather than issuing bonds for a specific ESG-oriented project, borrowers set ESG-related targets (largely based on Sustainable Development Goals) on prominent issues, such as social welfare, inequality, and environmental impact. ICMA has provided voluntary principles for issuing SLBs, which consist of five core components:

- Selection of Key Performance Indicators (KPIs)

- Calibration of Sustainability Performance Targets (SPTs)

- Bond characteristics

- Reporting

- Verification

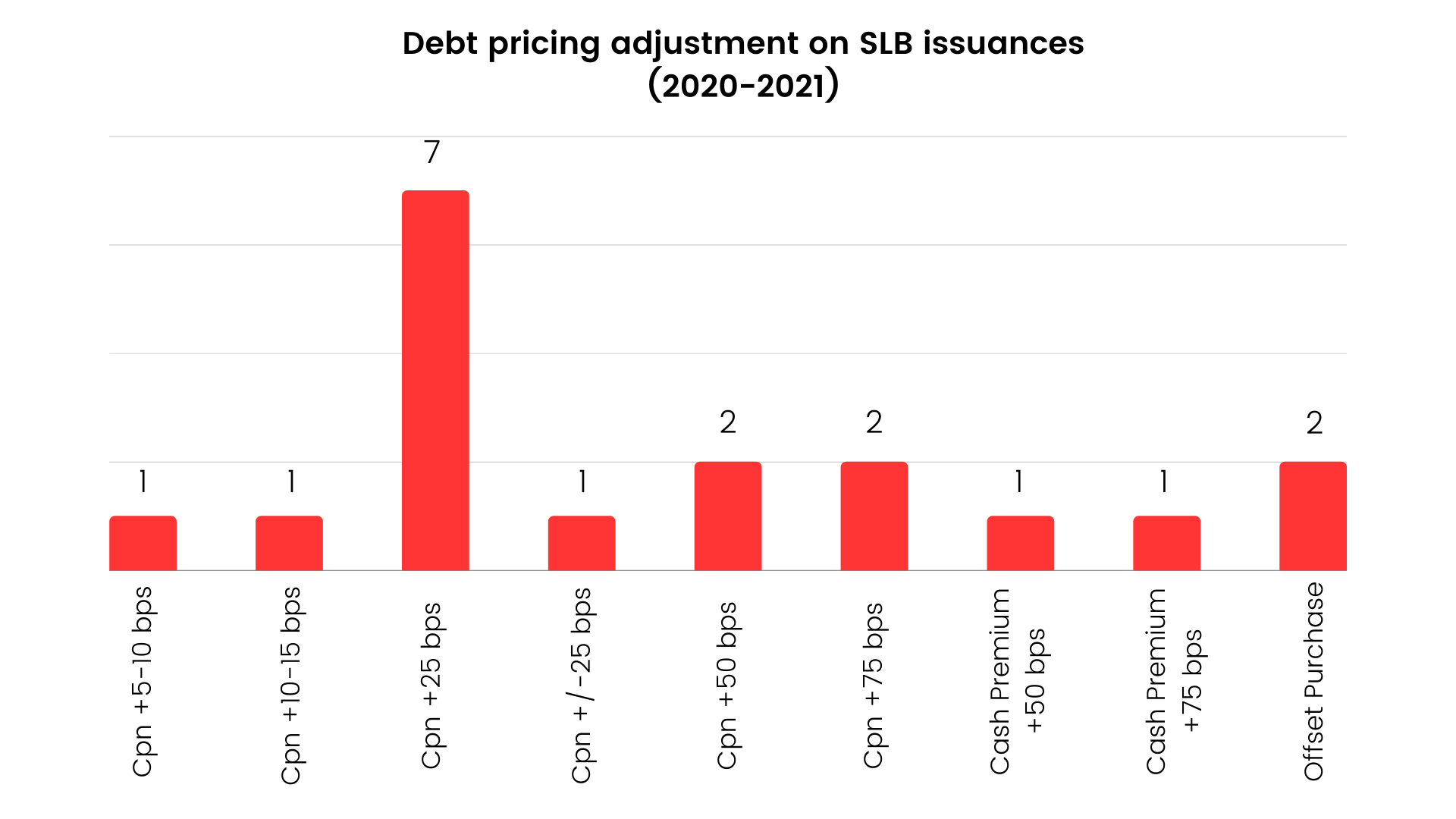

Enel, an Italy-based energy company, was the first to issue a target-linked bond, even before the announcement of SLBP. The bond offered a step-up coupon of 25bps that became the market norm in the early stages until France-based luxury fashion house Chanel adopted a step-up of 50bps and 75bps. As per S&P Global, a one-time 25bps step-up continues to be the most common debt pricing adjustment for SLBs if targets are not achieved within the timeline specified.

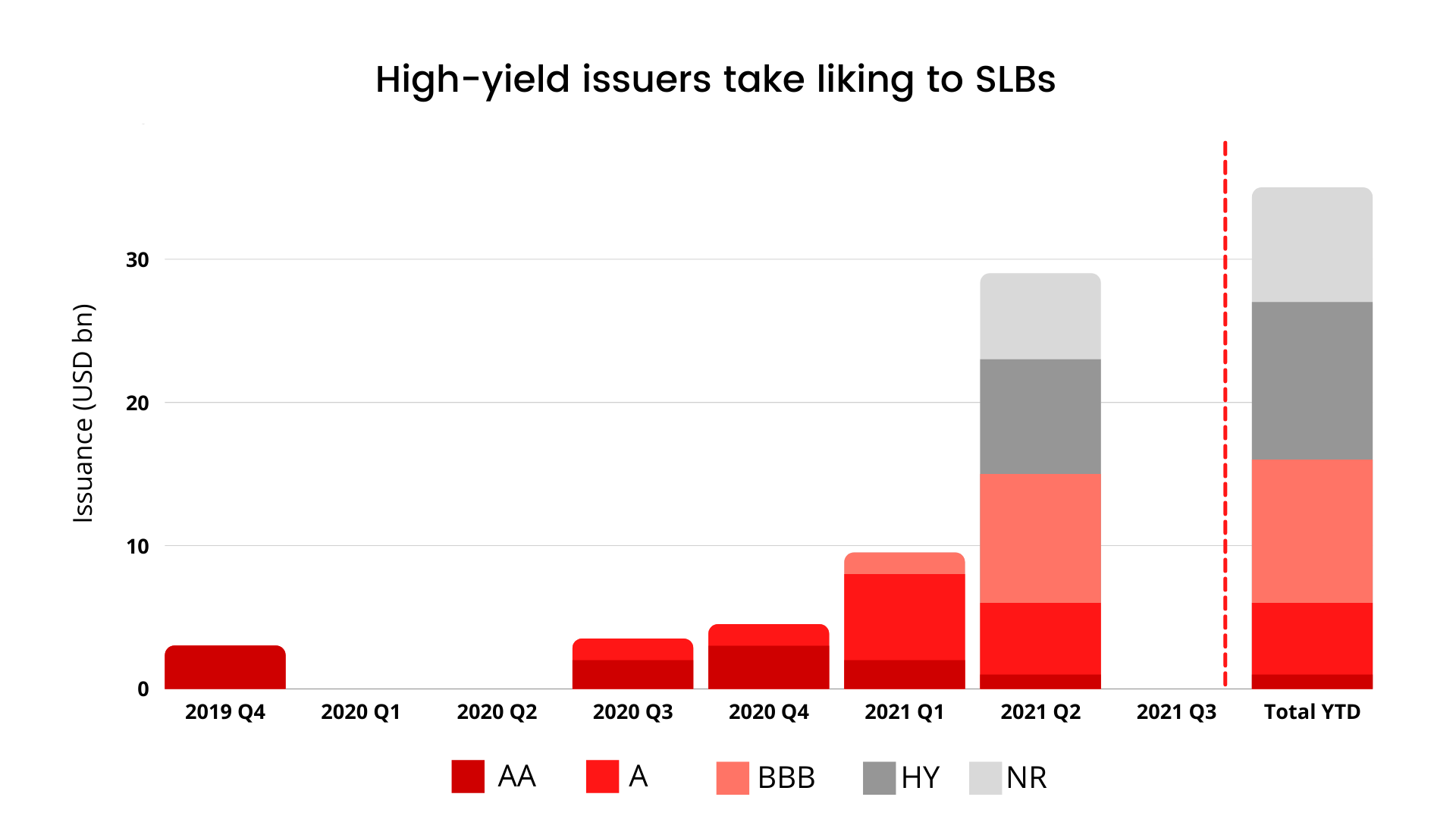

From the credit quality perspective, the SLB segment has also started to gravitate toward high-yield (HY) issuers. The flexibility in terms of use-of-proceeds amid lighter capital structure and lower prevalence than its investment-grade (IG) peers, makes SLBs a suitable option for these issuers. Moreover, improved accessibility and lack of disclosure issues for this type of debt financing have led to their increased adoption. Through the first half of 2021, one-third of the SLB supply came from the maiden HY category.

From the credit quality perspective, the SLB segment has also started to gravitate toward high-yield (HY) issuers. The flexibility in terms of use-of-proceeds amid lighter capital structure and lower prevalence than its investment-grade (IG) peers, makes SLBs a suitable option for these issuers. Moreover, improved accessibility and lack of disclosure issues for this type of debt financing have led to their increased adoption. Through the first half of 2021, one-third of the SLB supply came from the maiden HY category.

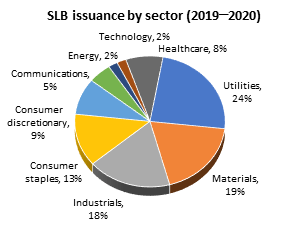

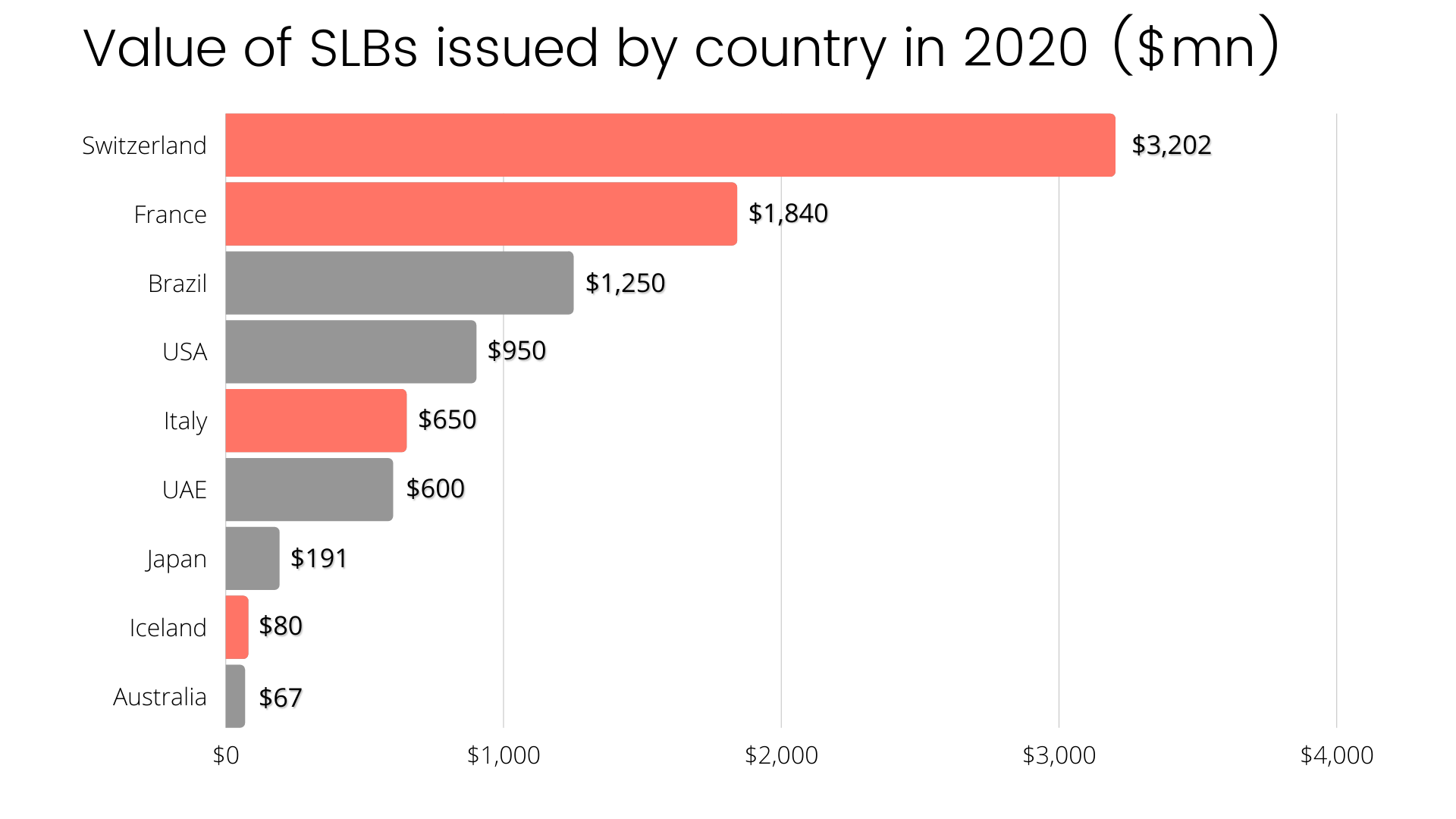

Unlike other sustainable debt instruments where identifying green-eligible projects may not be easy across all sectors, SLB’s structural flexibility allows for a wider issuer base than the conventional green bond. Such scale of adoption is evident from the host of issuers, such as ENEL, Suzano, Novartis, and Chanel, which were seen in 2020 and belonged to four varied sectors. So far, the harder-to-abate sectors such as utilities, industrial goods, and materials have been at the forefront in the SLB segment. Looking ahead, given that the structure could attract sectors that are hard to decarbonize, SLB issuances could gain significant momentum.

Pricing mechanism adjustment and advantages of SLBs

The sustainable-linked debt may have one of the three ways of pricing adjustment mentioned below:

(1) benefit mechanism,

(2) penalty mechanism, which are both a one-way mechanism, and

(3) both benefit and penalty mechanisms (two-way).

Under the one-way benefit mechanism, the issuer faces a margin discount if it meets its SPTs but would not face a penalty if it fails to do so, and vice versa for a one-way penalty mechanism. Under the two-way mechanism, the issuer will obtain a margin discount if it meets the predetermined SPTs and be charged a margin premium if not.

The fundamental advantage of SLBs over other sustainable debt options is that now even those issuers without any green or social capital expenditure planned can resort to sustainable financing. Moreover, being a performance-based forward-looking instrument, issuers that may still be in the nascent stages of their sustainability journey could see SLBs as an attractive option. Meanwhile, the lack of restrictions on how the proceeds are to be used could help impart operational and financial flexibility to the issuer.

On the flipside, critics of the step-up coupon see the structure as problematic as investors largely benefit when the company misses its target, making it a fundamentally irresponsible mechanism. Critics believe that the structure needs to shift from one that rewards bond holders to an ESG-friendly utilization that makes tangible progress toward sustainability. For example, the purchase of carbon offsets is seen as a way in which issuers could get away without ensuring a positive climate impact.

Regulatory boost to SLBs

From the regulatory standpoint, SLBs garnered an exceptional response in Europe after the European Central Bank (ECB) decided to consider them as eligible collaterals in their asset purchase programme (APP) and Pandemic Emergency Purchase Programme (PEPP) effective January 1, 2021. This inclusion enabled SLBs to be recognized as a viable tool for supporting corporate transition. To qualify as collateral, the issued SLBs must have one or more of the SPTs linked to either environmental objectives in the EU Taxonomy regulation or United Nation’s

Sustainable Development Goals relating to climate change or environmental degradation.

Source: Environmental Finance Source: S&P Global Ratings(Data through April 9, 2021)

Meanwhile, traction in the US too has picked pace and further growth could be witnessed as the Biden administration moves toward adopting new climate disclosures. Currently, the focus is on climate-related policies. It could be evidenced from the passage of the ESG Disclosure Simplification Act of 2021 by the US House of Representatives in June 2021, up for review in the Senate. If passed, a standardized disclosure of ESG metrics, as determined by a Sustainable Finance Advisory Committee, along with a discussion on metrics and long-term business strategy would be included in an issuer’s SEC filings. Furthermore, the legislation includes disclosures related to political contributions, executive compensation, climate risk, workforce demographics, and cyber security. It would enhance transparency and prove to be beneficial for both issuers and investors.

The path ahead

In the coming years, as more firms tap into the ESG debt market, SLBs could become the new favorite. Although growing at an exceptional pace, the market remains nascent and is likely to find its footing alongside the traditional use-of-proceeds ESG debt instruments. In fact, they are likely to complement the traditional sustainable bonds; one offers a forward-looking approach to an issuer’s strategy while the other could help identify concrete investments that will be made to achieve targets. Moreover, ICMA’s SLBP followed by over 80% of SLBs in 2020 has promoted and enhanced the market discipline. New frameworks such as the EU’s green taxonomy, scheduled to come into effect in 2022, will further improve credibility and enable standardization of SLBs.