Nord Stream 1: A lifeline for European gas till now

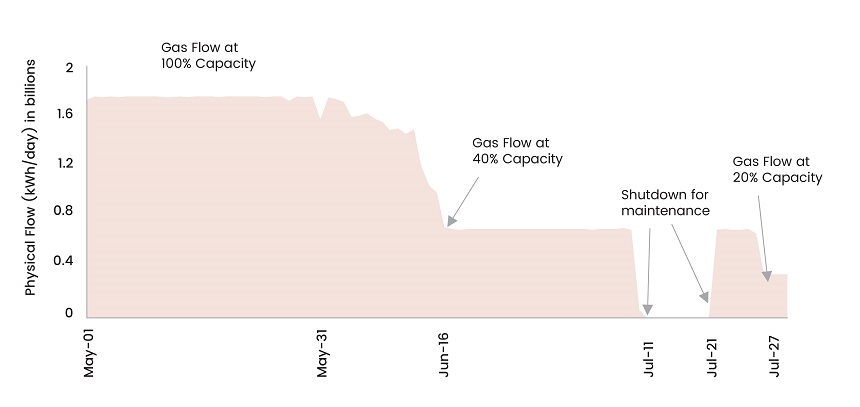

On 27 July 2022, the gas flow from the 1,224km underwater Nord Stream 1 (NS-1) pipeline, starting from Russia to Europe, was reduced to just under 20% compared to its full capacity, citing issues with a turbine. Earlier, the NS-1 was shut down for 10 days, from 11 July to 21 July 2022, for regular maintenance work. With the mounting number of sanctions against Russia on account of the Russia-Ukraine war, uncertainty about the future gas supply lingers. Russian supplies contribute about 35–40% of Europe’s natural gas requirement, which is mostly transported through the NS-1 pipeline.

Germany is heavily dependent on Russia for gas supply. In addition, Italy, Austria, and Central and Eastern Europe also consume a huge volume of gas supply from Russia. Due to the constantly rising energy and commodity prices, gas prices have already surged by 70% in Europe since Gazprom, a Russian state-run oil and gas company, slashed supply by 60%. In June 2022, Reuters stated that a complete stop of Russian gas would cost Germany 12.7% of its economic performance in the second half of 2022. This would translate to EUR193bn in total economic losses to Germany. The situation with other European countries is similar. Hence, further supply cuts could trigger a recession across Europe going into the next year.

Figure 1: Nord Stream 1 Recent Supply Movement

Source: Nord Stream AG

Turbine story: A Blame Game to Keeping Europe Gas Starve

In June 2022, citing the delayed return of a turbine, Gazprom reduced gas supply by 60% compared to its full capacity. The gas flow was not only stopped for Germany, but huge volumes were also curtailed for other routes linking Russia to Slovakia, the Czech Republic to Austria via Ukraine, and Belarus to Poland. The NS-1 pipeline transports 55 billion cubic metres (bcm) of gas annually from Russia to Germany under the Baltic Sea. The turbine required for the functioning of NS-1 was being serviced in Canada by Siemens. After the regulatory and sanctions-related tussle between Europe, Russia, and Canada, on 10 July 2022, the Canadian government allowed the transport of turbines through a time-limited and revocable permit for Siemens. Under this, one turbine was transported from Canada, and the other five turbines will be repaired at Siemens, Canada, over the next two years. After overcoming the regulatory hurdles, the turbine was finally delivered to Gazprom. However, as per Gazprom, the turbine repair work was not in line, which ultimately forced the gas supply to just 20% in late July 2022 as compared to the May 2022 levels. With the worsening current geopolitical tensions and the mounting number of sanctions, there is a lot of a grey area around the resumption of gas flow at full capacity to Europe, which was further exacerbated by the recent supply cuts.

Gas Inventory Levels: Europe’s Winter Goals too Ambitious at One-fifth of Gas Flow Capacity

Europe is planning to stock up to 80% of gas storage by 01 November 2022 to create a sufficient buffer against the winter. Germany is aiming for a higher goal of stocking 95% gas supply by the same date. Even if the 80% target is reached, it still would not be enough to get countries through winter without continuous supplies of more gas. The storage capacity and storage levels differ vastly among European countries. Whilst countries are lining up to fill their storage capacities, even at full capacity, Spain, Portugal, Bulgaria, and Croatia would run out of gas by December this year.

If Russia continues to supply gas at 20% capacity, the stated goals would not be achieved, thereby adversely impacting the European economy. The Dutch wholesale gas price for August, the European benchmark, was up by 7% at EUR210 per megawatt hour in July 2022, which is up by around 400% from the same time last year. The soaring energy prices are already putting pressure on inflation, thereby squeezing the spending power of people and further pushing the regional population towards poverty, which has been a concern since the COVID-19 pandemic.

Germany: Putting its Neck on the Line as Winter Looms

Nearly half of the German households rely on gas heating during the winter season, which is from October to March. If the gas flow is not restored at its full capacity, it will create a catastrophic problem for Germany to fill its gas storage by 80% through October and 95% by November. As per the data from Gas Infrastructure Europe for July 2022, the German current gas storage levels are only two-thirds full. Although the storage capacity of Europe is massive, the demand is equally huge. At the current capacity, the German tanks can hold only 108 days of consumption.

Gas storage activities have ramped up, especially in the second half. However, with just one-fifth of the Russian gas flow through NS-1, Germany remains behind in its goals of storing 95% gas for winter. Hence, the government has embarked on an emergency gas plan. Household and essential services remain the top priority under the plan. E.g. the city of Hanover, Germany, decided to turn off warm water in the showers of its pools and gyms along with municipalities from the last week of July 2022.

Figure 2: Gas sales by customer group for 2021 (data in billions of kilowatt hours)

.jpg)

Source: Reuters, Zukunft Gas

On the industry front, chemicals, metals, and foods remain highly exposed to gas shortages. As per Moody’s, BASF alone consumes about 4% of Germany’s gas. The aluminium industry, where energy costs form about 40% of production costs, relies heavily on gas for smelting. Currently, Germany employs over 60,000 employees and generates EUR22bn from the aluminium industry. Reducing gas supply by only 30% could lead to 50% of the idling capacity for this industry. The paper industry, which generates about EUR15–16bn of revenue with 40,000 employees, again relies on gas. Likewise, steel, glass, and other commodity-led industries are on the verge of decline, which will produce a ripple effect on the economy, leading to a recession. Overall, the gas halt may impact more than 5 million employees directly or indirectly.

Figure 3: Gas consumption by industry (2021)

.jpg)

Source: Zukunft Gas, The Economist

European Alternative Measures to Circumvent the Gas Crisis: Ongoing Efforts do not Seem Enough

Whilst some EU states, such as Poland and Lithuania, have stopped gas imports from Russia, Germany has increased it. As per Reuters’ report dated July 2022, Germany received 32% of its total natural gas supplies from Russia in 2011, which increased to 52% in 2021, despite formal sanctions on Russia. Germany being the largest Russian gas consumer in Europe, could import gas from Norway (the second biggest exporter to Europe after Russia), the UK, Denmark, and the Netherlands through the pipeline in the absence of Russian gas flows. Germany is already negotiating with the world’s top LNG suppliers, including TotalEnergies and Shell Plc, for alternatives. Europe is already tapping the US and Canadian markets for gas supplies via ships, but this route is way more expensive compared to the Russian supply route. Interestingly, a high single-digit percentage decrease in gas demand was seen in May due to the ramp-up of renewables, increased coal power generation, and lower demand owing to lower GDP growth. Germany is also considering extending the life of the Bavarian Nuclear Plant and reversing a decision to shut the Isar 2 facility in Munich.

Other Options: There are, but not as Cheap as NS-1

Norwegian and US gas: Whilst supplying gas to Europe, Norway stands second after Russia. Norway is already pushing gas production since the war to help Europe for ending its reliance on Russian imports. The US also started to supply 15bcm of gas to Europe this year, but the number is lower compared to the 2021 consolidated consumption level of 155bcm. Additionally, the gas transport from the US via ships will add to extra cost.

Moving to coal: Utilities and a few other industries that can switch to coal or oil are already in talks to secure supplies. But by this route, Germany’s ambitions of energy transition towards emission-free fuel by 2030 will be delayed. However, the same option is not available to everyone. One of the leading steel companies, ThyssenKrupp stated that an alternative option barring gas is not possible, and the plants may have to be shut down.

Emergency plans: If Germany is forced to implement an emergency plan, household consumption will be prioritized along with hospital and essential services. However, this will result in halting the operations of the biggest companies in the country, leading to a series of downgrades. The government is already planning for more drastic measures, including gas rationing for energy-intensive industries, such as steel and agriculture. These measures are listed under ‘Save Gas for a Safe Winter’ and are part of a European-wide gas demand reduction plan, which is aimed to reduce gas use by 15% until next spring.

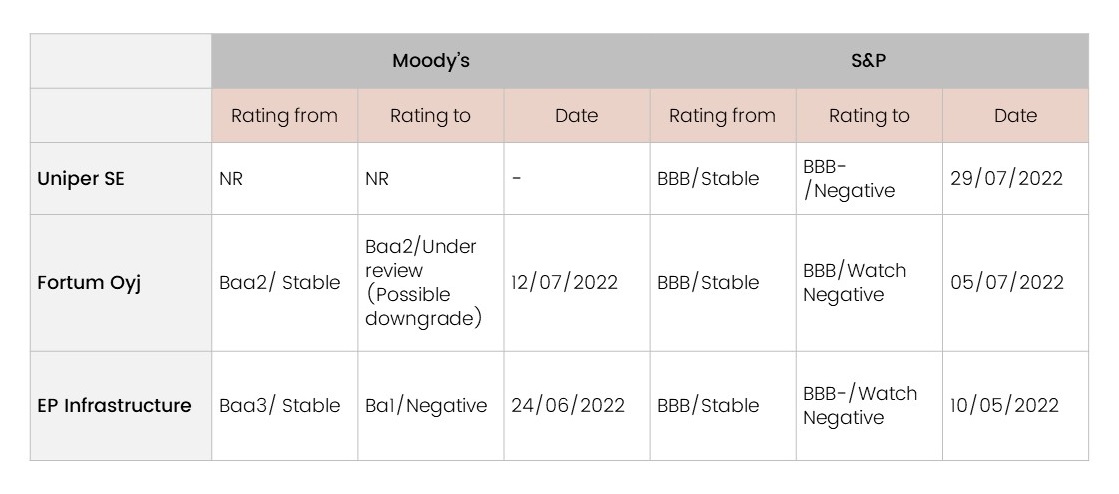

Impact on European companies: Downgrade risks on the horizon

Uncertain and costlier gas supplies are deteriorating the credit quality of European utilities. Recently, Uniper SE was downgraded by S&P to BBB- from BBB with a negative outlook, owing to the Russian gas import cut. Gazprom accounts for 50% of gas imports for Uniper SE, which was already reduced to 40% earlier this year. In July 2022, Uniper SE already reached out to the government and received EUR15bn in a bailout package. Below are the few rating actions that were taken by S&P and Moody’s on European utilities.

Table 1: Credit rating actions by the Rating agencies

Source: Moody’s and S&P Global ratings

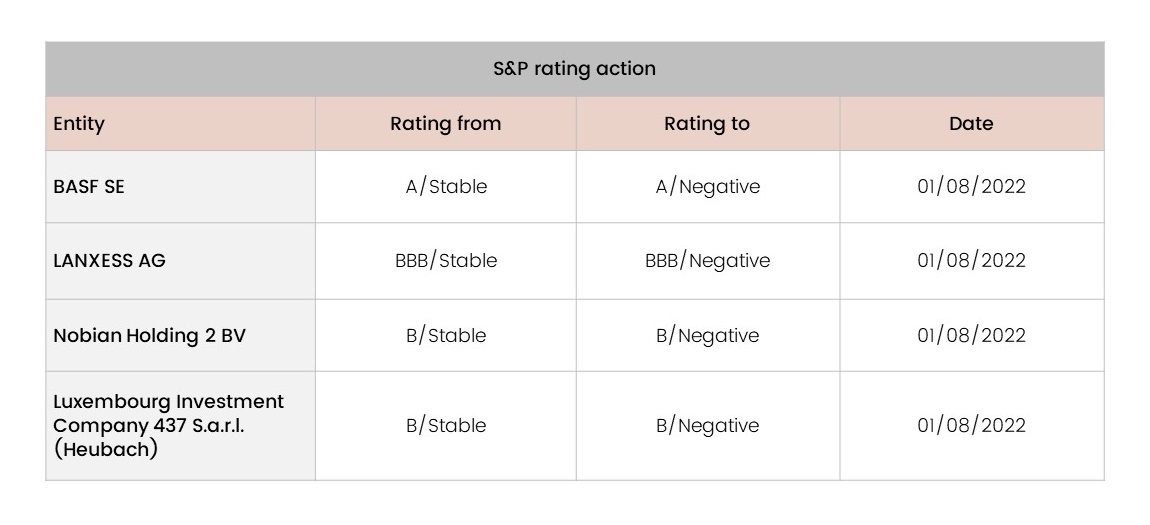

With the soaring gas prices, S&P took several rating actions on European chemical companies on 1st August 2022.

Table 2: Credit rating actions by S&P Global Ratings

Source: S&P Global Ratings

If the current conditions persist, European utilities could take a material hit as earnings and liquidity would deteriorate amidst higher energy prices. This, in turn, could lead to additional rating downgrades, and most importantly, fallen angel risk could increase. Although government support is likely to provide comfort, credit negative actions are imminent. Even the best-intentioned emergency plans to deal with a potential stoppage of Russian gas supplies—primarily rationing but also passing on ascending costs to the end consumers—may fail to avoid having social consequences. Hence, the German government needs to manage these risks quickly and proactively.

Impact on the Russian economy: Economic losses quietly compensated through China

Gazprom contributed about 3.2–4.6% to the Russian GDP from 2017 to 2020. NS-1 contributes about one-fourth of the total gas supplies to Europe. Although the repercussions are material to Russian GDP as well, Kremlin seems to absorb or ignore this blow on the back of the ongoing geopolitical tensions and seemingly aims to bring Europe to the table for discussion ahead of the winter season.

Russian Central Bank’s Governor Elvira Nabiullina said that Russia would supply crude to countries that are willing to cooperate rather than to those that impose a price cap on Russian oil. Interestingly, Russian gas supplies to China were up by 61% via its Power of Siberia pipeline. It seems that Russia is compensating for the loss resulting from the reduction of gas supplies to Europe by diverting its oil to Asian economies. The European Union also allowed Russian state-owned companies, Gazprom and Rosneft, to ship oil to third countries. While the arrangement is not likely to reverse the economic losses the government is incurring by not supplying gas to Europe, it certainly gives more power to Russia when it comes to negotiation with Europe.

With a presence in New York, San Francisco, Austin, Seattle, Toronto, London, Zurich, Pune, Bengaluru, and Hyderabad, SG Analytics, a pioneer in Research and Analytics, offers tailor-made services to enterprises worldwide.

A leader in Market Research services, SG Analytics enables organizations to achieve actionable insights into products, technology, customers, competition, and the marketplace to make insight-driven decisions. Contact us today if you are an enterprise looking to make critical data-driven decisions to prompt accelerated growth and breakthrough performance.