The European banking sector has been under stress over the past few years owing to various factors such as low interest rates, massive fines, and feeble earnings results. Further, high levels of bad loans continued to be a drag on the European banking system. According to KPMG, the European banking sector has around €1.1trillion (£0.94tn) in non-performing loans, almost three times as much compared to the US. Besides high volume of bad loans, banks are grappling with weak balance sheet strength and inadequate loan loss provisions. All these factors have collectively crimped the performance of European banks. Top banks such as HSBC Holdings, Deutsche Bank, and Barclays have all come up with disappointing earnings results. This is in stark contrast to big-ticket U.S. banks, that are benefitting from a contractionary monetary policy. U.S. players such as J.P Morgan, Citigroup, and Goldman Sachs have posted stronger-than-expected profits in 2016.

Retail Banking – PSD2 – Game-changing Directive

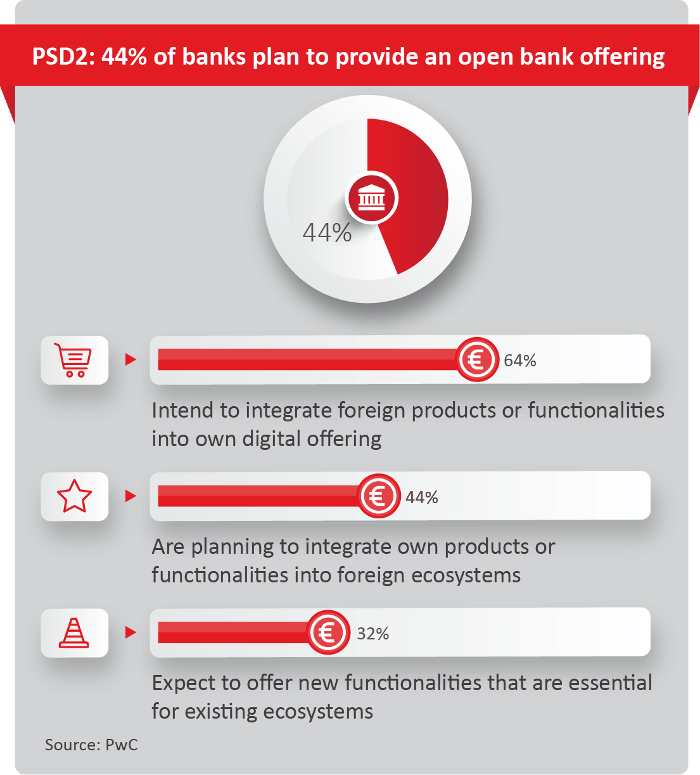

The banking sector clearly has a tough road ahead, but structurally, it is poised for a massive overhaul. The European Commission is moving toward implementing the revised Payment Services Directive (PSD2) by January 13, 2018. What is the PSD2 all about and why it has generated so much buzz in the European banking sector? Well, PSD2 is widely seen as a ‘game-changing’ directive. Many expect it to end banks’ control over their customers’ account information and payment services. It also offers third-party providers access to customers’ accounts through open application program interfaces (APIs). PSD2 has a widespread impact on the financial service industry, banks will need to re-strategize their digital offerings and product portfolios.

This eyeball-grabbing directive is aiming to transform the payments landscape across the European Union. PSD2, once implemented, will pave the way for bank customers (both consumers and businesses) to use third-party providers to manage their finances. A likely scenario could be that of customers using Facebook or Google to pay their bills, making person-to-person payments (P2P) transfers with their money safely parked in their respective bank accounts.

PSD2 – administered by the European Commission – aims to ensure every EU bank is digitally optimized. In a nutshell, this directive will create cut-throat competition in the payment services market in Europe between banks and new payment service providers (PSPs) as well as drive innovation in the European Fintech industry. More importantly, it will eliminate hidden fees charged by banks. There is a notion that banks find it convenient to add transaction fees. However, now with the market becoming more crowded, banks will have to put their ‘rethinking’ caps on. All these factors will go a long way in ensuring an improved customer experience.

Why are bankers worried about PSD2?

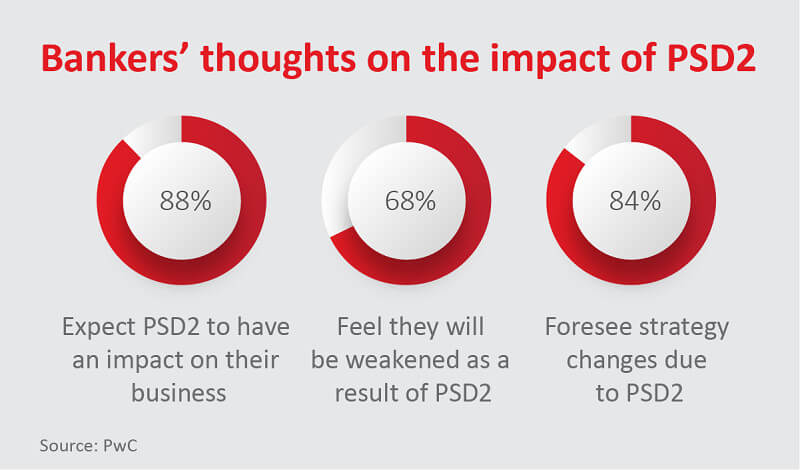

In fact, the perceived fierce competition in the banking sector is a big worry for most European banks. According to some estimates, 20-25% of banks could be at risk from the new competitors owing to PSD2. Furthermore, PSD2 is also raising operative and legal concerns.

Would banks’ monopoly end?

The advent of PSD2 has triggered talk about whether it would mark the end of banks’ monopoly over customers’ accounts. Delving deep, it is reasonable to assume that banks are unlikely to lose their significance as far as catering to customer needs are concerned, while granting third-party providers access to customers’ account information. The need of the hour for banks is to walk down the ‘reinvent’ path and come up with robust differentiators to stay competitive.

The host of regulatory approvals and licenses in the banking space means that it is never an easy proposition for new entrants. But non-banking FinTech companies, by virtue of PSD2, could find it a lot easier to foray into the market and play a significant role in the future financial landscape.

Investment Banking – Will MiFID II Be A Devil or Angel?

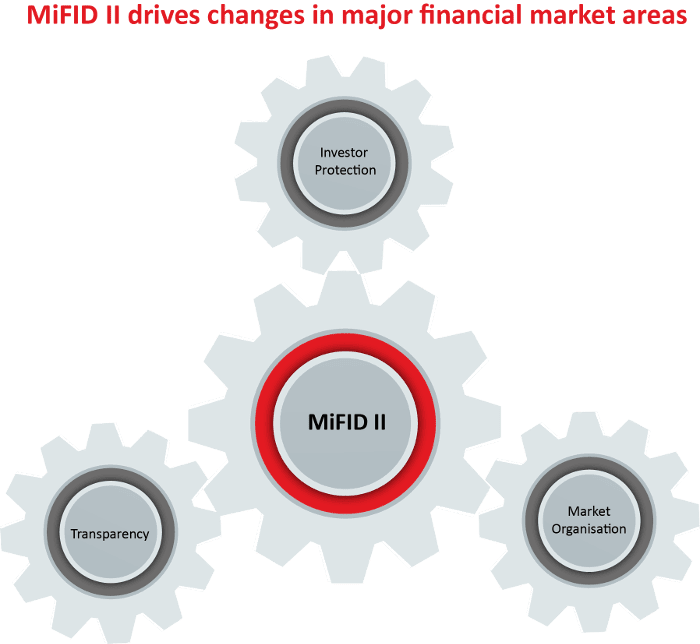

The European banking sector is also bracing up for the second installment of the Markets in Financial Instruments Directive (MiFID II). MiFID II is considered one of the European Union’s most ambitious financial reforms. MiFID II is created to regulate and steer various aspects of the financial service industry, such as:

- OTC derivatives and commodity trading

- Investor protection and provision of investment services

- Transparency

- Miscellaneous

- Supervisors

- Authorization and organizational requirements

- Development in market structure

MiFID II will come into force in 2018. The challenges of complying with it lie in preparing asset managers for so-called unbundling. Under Mifid II, asset managers are required to budget separately for broker research costs and trading costs. This is a significant departure from the decades-old tradition of bundling together trading and broker research costs into a single fee. Prior to MiFID II, asset managers received research from investment banks or brokers in exchange for carrying out trades through them. Asset managers have two options – either they absorb their research costs or set up a research payment account.

MiFID II is likely to hit investment banks in the future. A research conducted by Electronic Research Interchange (ERIC) revealed that 74% of asset managers foresee a reduction in investment bank research. With MiFID II, regulators expect to improve the quality of research. For instance, if there are more than 400 reports generated for a particular stock, we can end up having a scenario of 50 reports or even less for that stock. This will further enhance requirements for in-depth bespoke research.

Conclusion

The effective implementation of PSD2 and MiFID II is of crucial interest to the European banking sector. These directives will crank up competition in the banking sector, which in turn, will drive consolidation across the European Union. It will also improve the customer journey. For sure, PSD2 and MiFID II might pan out to be a short-term pain but would pay rich dividends in the long run.

SG Analytics provides customized research solutions to the investor community. In the case of any research queries, please feel free to get in touch with our Lead Analysts:

- Steve Salvius – Investment Banking Support

- Mayuresh Wagh – Equity Research

- Amit Bansal – Fixed Income and Credit Research